2024-01-15

Today, I started reading 'The Outsiders.' In this post, I will solely focus on some specific tactics I noticed because, as Atul Gawande said, it's natural that we should study these outliers in order to learn from them and improve performance.

I will focus on the second one

Think of this as a toolbox.

”Stated simply, two companies with identical operating results and different approaches to allocating capital will derive two very different long-term outcomes for shareholders”

This is Warren Buffets point of this:

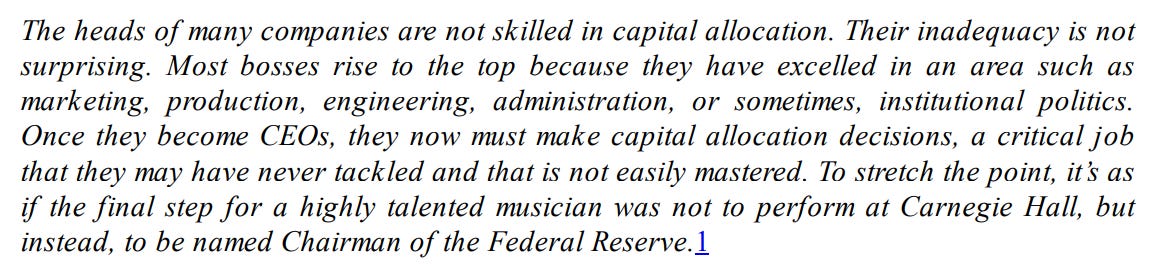

He also talks about the 'institutional imperative,' in which most CEOs act like teenagers under peer pressure, where CEOs are inclined to imitate the actions of their peers. This summary will focus on several best-practice capital allocators and their toolbox. All of these CEOs understood these principles

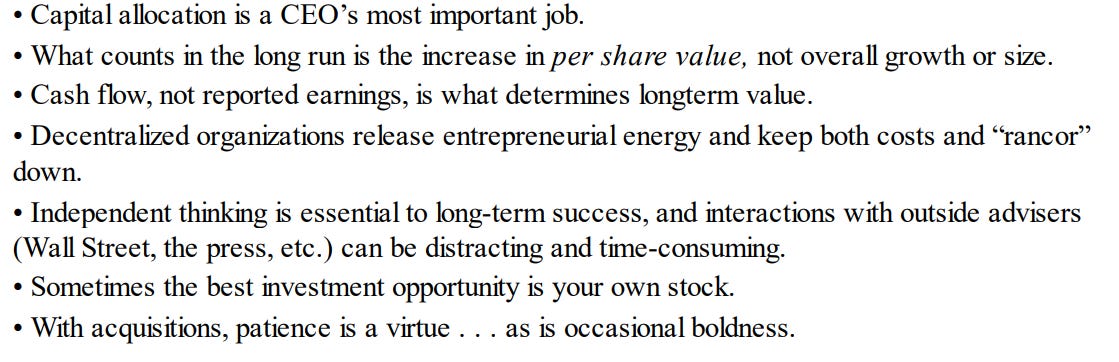

I copied the paragraph below due to its importance:

“At the core of their shared worldview was the belief that the primary goal for any CEO was to optimize long-term value per share, not organizational growth. This may seem like an obvious objective; however, in American business, there is a deeply ingrained urge to get bigger. Larger companies get more attention in the press; the executives of those companies tend to earn higher salaries and are more likely to be asked to join prestigious boards and clubs. As a result, it is very rare to see a company proactively shrink itself. And yet virtually all of these CEOs shrank their share bases significantly through repurchases. Most also shrank their operations through asset sales or spin-offs, and they were not shy about selling (or closing) underperforming divisions. Growth, it turns out, often doesn’t correlate with maximizing shareholder value. This pragmatic focus on cash and an accompanying spirit of proud iconoclasm (with just a hint of asperity) was exemplified by Henry Singleton, in a rare 1979 interview with Forbes magazine: “After we acquired a number of businesses, we reflected on business. Our conclusion was that the key was cash flow. . . . Our attitude toward cash generation and asset management came out of our own thinking.” He added (as though he needed to), “It is not copied.””

The 8 post that will follow (not directly after each other) will focus on several best-practice of each capital allocators and their toolbox. In Part 9 i will summarize.

Thanks,

Finn