2024-02-15

I'm trying to get into volatility trading and the first thing you need to understand is how to value options with a model. It's impossible to find a model that 100% accurately reflects the price of an option; the variables are just too complex. The map is not the territory.

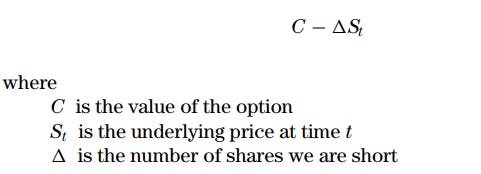

To get mispriced options, we need to approach the model backwards. First, we assume that the trader holds a delta-hedged portfolio, consisting of one call option and a delta amount of stock sold short.

Some known facts:

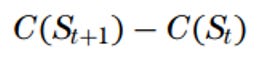

With this formula, we are delta neutral. Now, over time, the underlying changes, which we define as St+1. To define the change for C, it is now...

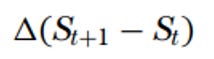

and for delta St it is now

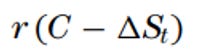

Now, we also need to add any financing charges we incur for borrowing the money we need for our position. This is defined as...

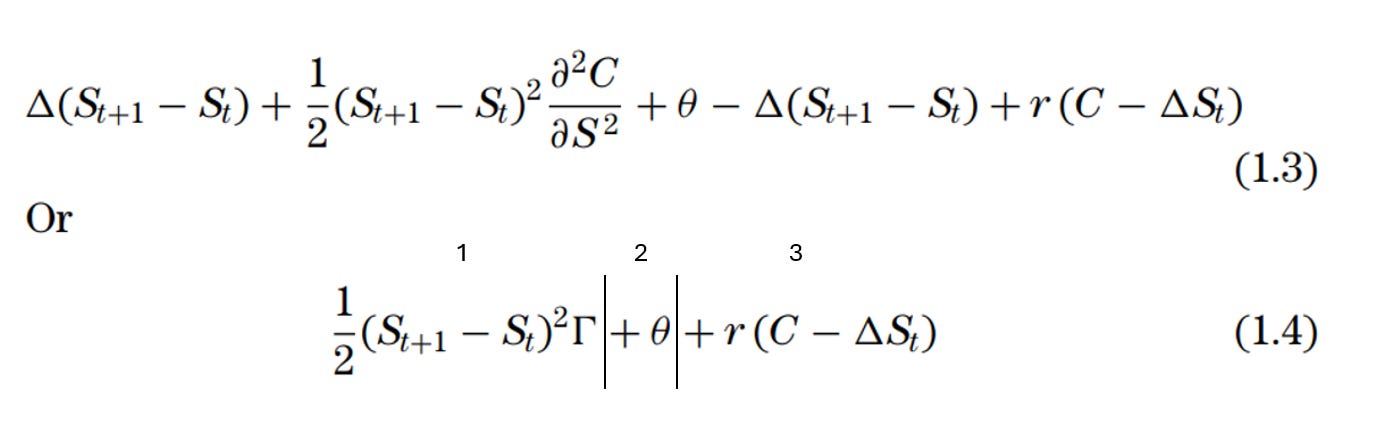

In total:

Now we try to estimate the price of the option by using the change of the underlying through second-order Taylor expansion

The first term is the gamma and is proportional to half the square of the underlying price. The second is the theta; the holder loses money with the passing of time. The third term gives the effect of financing. Holding a hedged long option portfolio is equivalent to lending money.

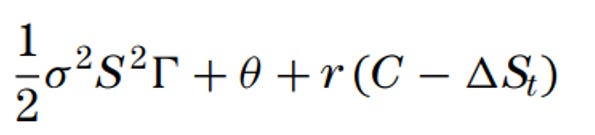

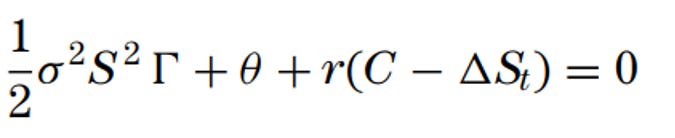

Sigma is the standard deviation of the underlying return, known as volatility, so we can rewrite it as...

We can set the equation to 0 because it is riskless and we finance it with borrowed money.

Now, the price change is not in the equation, but is being expressed through sigma or volatility. You might say that we need to include the drift, but it does not matter due to it being hedged away by the right amount of shares. You can use the equation for European, American, or even exotic options. We have two options when going on:

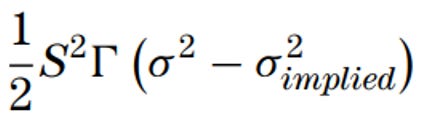

If we estimate the volatility and it differs strongly from the volatility implied by the option market, we have a trade. We buy the option and hedge by selling the stock. Our profit will be the difference between the implied volatility and the forecasted volatility if we are right.

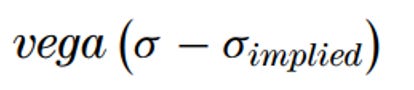

You can think of this as Vega, which is how much an option price changes when the implied volatility changes from, let's say, 18% to 19%. In other words, the profit of a hedged option.

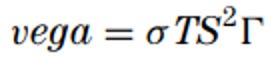

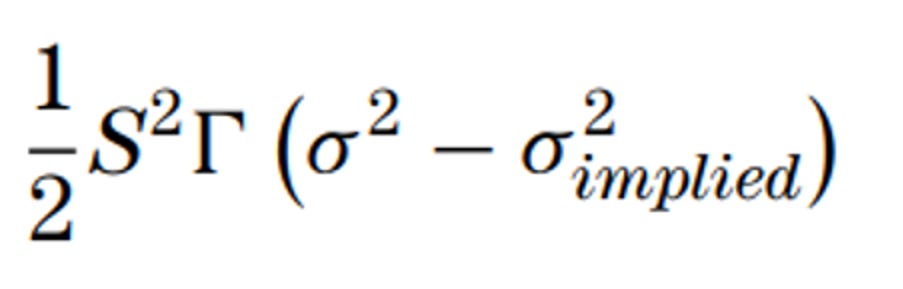

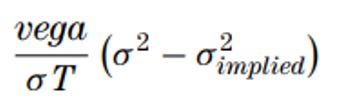

Now, if we hold the option and the realized volatility is sigma, we will make this amount of Vega profit. Now note that we need to rebalance our hedge from time to time. This can be accounted for by noting the relationship between Vega and gamma.

or

now being

The Black-Scholes-Merton model is only useful for controlling the fast-moving option price as a slow-moving parameter, which is the implied volatility; it is not for risk control. We also need to be aware of black swan events that supposedly never happen. This tail risk can be taken care of by either buying out-of-the-money options or keeping individual position sizes small. But generally, we get paid for taking risk. So never use the model for which you assumed the price for assuming risk.

Always remember that our model is not an accurate reflection of reality:

Most of this is from the book Volatility Trading

Thanks,

Finn