2024-02-25

In this post i will go through each step to get a commerical loan from a bank

Initial Meeting:

Second Meeting:

Outstanding Loans: How many other loans does the business have? How long have they been outstanding? What is the outstanding principle? What is the historical payment record? How much interest has been paid?

Cash Flow: Provide further information to enable them to normalize the cash flow. For example, annual salaries or bonuses, CAPEX.

Outlook: Offer them an outlook on what you want to do and present your story in detail.

Level of Equity "Skin in the Game": Banks want to see a certain amount of equity to ensure that you have "Skin in the game." Equipment: 0-10%, Real Estate: 20%-30%, M&A/MBO: 20-40%.

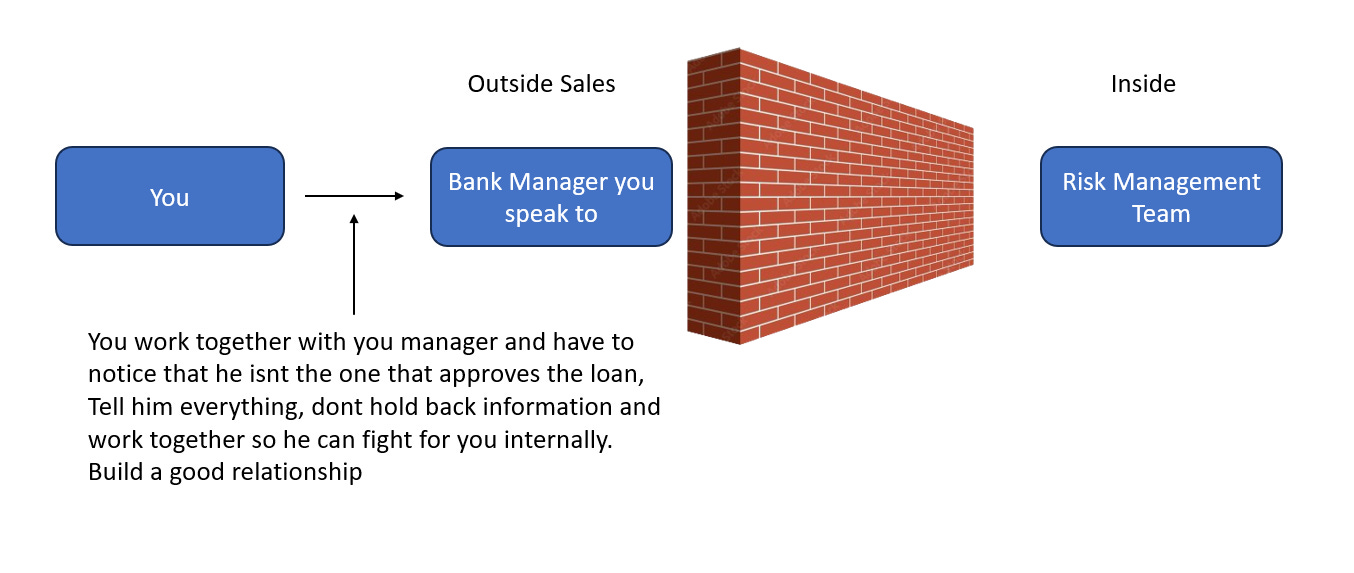

They take the information and create an internal file to analyze if you can borrow this amount. Personal Net Worth? Other assets? Cash flow of the business? Only really basic, maybe 2-6 hours. They ask, "Can this get approved by the risk team?" Note: the bankers at this stage are salespeople; they are trying to sell the debt to you, often having to meet budgets they have to fulfill per year. They want you to borrow as much as they can.

Preliminary deal reviews (possibility):

If there are some challenges with your loan, there might be the possibility to submit a "first look" sheet with your commercial banker to the risk team. This can save you time and is around 2 pages long, summarizing the business, target customer base, competition, value add, management team, employees, historically financial performance, and documentation of the proposed debt transaction.

If they are comfortable, they will give you a termsheet, which is nonbinding and communicates from the banker to the borrower what they will offer. The Borrower will receive this and negotiate with the bank and later signs it as well, stating that they will only work with this bank. I will make another post on how to negotiate a term sheet.

In this stage, the bank will tour the facility, understand the sector competitors, and grasp the business. This will still be done by the banker, and they will submit the file to the internal risk management team.

This can take several weeks. Some tips:

The risk management team will look at the file in a more detailed manner. They are not sales-oriented and are basically the defense. They may ask for more security or more information on pricing, competition, basically anything. They will then approve the Term Sheet. This can take up to 5 days, and they can ask further questions. If they decline the deal, you can ask the banker to refer to another lender that would do the deal or renegotiate the term sheet (reduce leverage, increase equity, increase interest rate). Most of the time, a decline is outlook-related and very specific; ask why? If they accept, the legal team will work on the Offer of Finance.

This is the document that the legal team will give you; it is binding, and you commit. Some banks even offer to close the offer of finance on the day of closing an M&A deal.

<$2MM loan = $7,5k-$10k fee

>$10MM+ loan = $15-25k

Cost increases relative to the complexity and number of parties involved.

Try to work with tier 2/3 legal firms; the brand name does not matter. And use lawyers from local offices.

Quarterly Annual Reviews: Prepare a summary of how you performed with some financials, but also add what you did and what you will do in the future.

Dealing with turnover: If your banker changes, take time to talk to the new banker on your file and encourage them to remain an internal advocate.

Site visits: Some banks want to visit the business sites annually to ensure that everything is funded as it should be.

Communicate your story: Bankers deal with a lot of people, and your "story" can be forgotten. Tell them about future lending opportunities and have patience; maybe even take them out to lunch. You never know when you might need their favor.

Get you connected, can provide many term sheets, have better connections, will walk you through the lending process.

Cost: Small upfront retainer (10k) and then once the loan is funded as a percentage of the loan value, between 2-5% for <$10M and 1-2% for $10M+.

Who should use loan brokers:

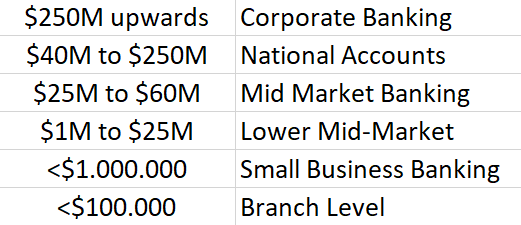

Always ask the bank if you are in the right division for your lending amount. What is your target range?

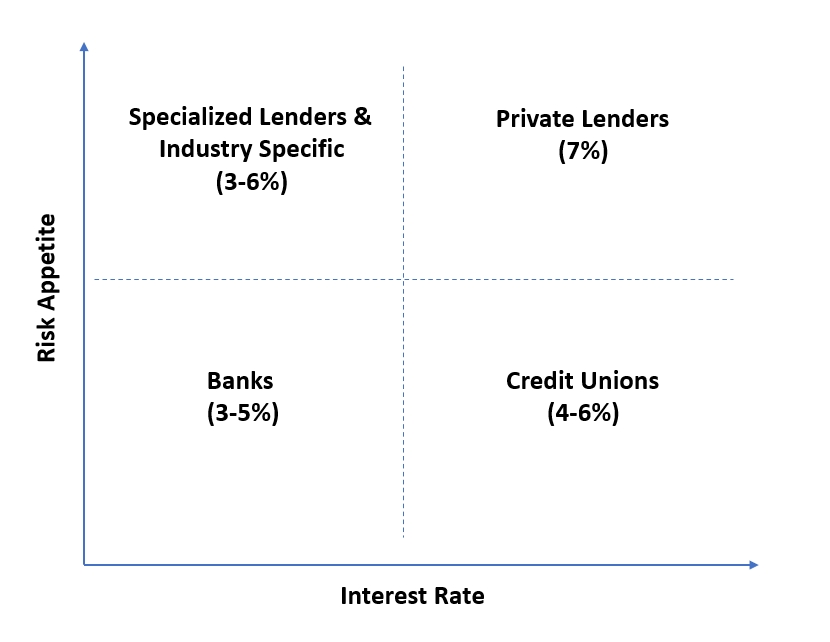

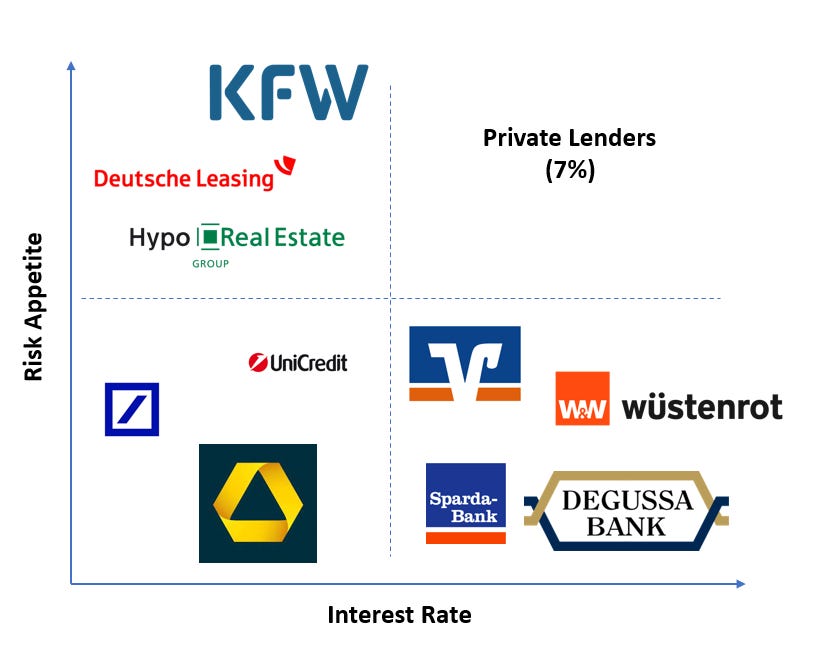

Banks: They prefer A clients—those with substantial size and robust cash flows.

Private Lenders: Assume more risk but offer higher interest rates.

Credit Unions: Positioned between Banks and Private Lenders, often serving community businesses or rural areas.

Specialized Lenders: Cater to niche markets such as automobiles or planes, providing competitive products for specific industries.

Thanks,

Finn